A CTO in Singapore sits across the boardroom table, presented with a question that could shape the company’s future: “Are we fully compliant?” – and are we building this next phase on the right foundation?” Rather than discussing the newest frameworks or programming languages, the discussion points focus on trust, regulation, and whether the fintech development partner chosen to lead the next build can withstand scrutiny from the Monetary Authority of Singapore (MAS), as Technology Risk Management (TRM) expectations become more stringent.

Choosing a development partner has a direct influence on the company’s license, reputation, and valuation. A wrong choice leads to regulatory exposure and architectural debt. The right one becomes a competitive advantage.

This guide outlines how CTOs should evaluate fintech software development partners in Singapore – with a practical framework tailored for 2026’s customized realities.

Start With Regulatory Depth, Not Code Samples

Within Singapore’s stringent financial ecosystem, having strong coding skills alone is not enough. Your fintech development services partner must understand financial compliance requirements specific to Singapore.

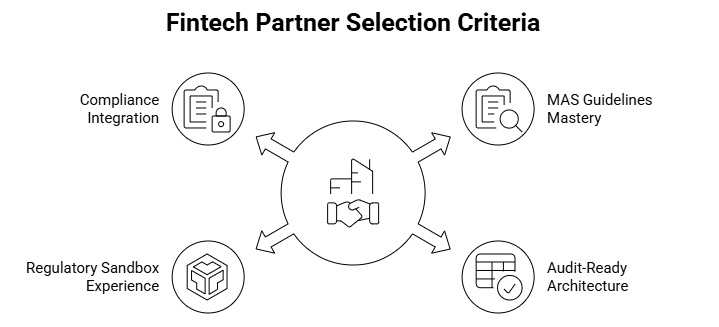

- MAS Guidelines Mastery: Ensure your fintech app development partner has a good grasp of the Payment Services Act (PSA) and MAS’s FEAT Principles for AI. This indicates their ability to build systems that are fair, transparent, and accountable – not just functional.

- Audit-Ready Architecture: A mature partner should demonstrate how they build audit trails and immutable logs directly into the transaction flows, rather than treating them as post-launch features.

- Regulatory Sandbox Experience: Ask whether they have helped companies participate in the MAS Regulatory Sandbox. This shows they understand how to test fintech products safely under regulatory supervision and launch them properly afterwards.

The main concern to be aware of here: a partner who views compliance as an afterthought rather than an architectural input. Fixing security and compliance gaps at the end of development costs much more than including them from the beginning. It is far cheaper and easier to plan them on day one than to manage issues later. A partner who is capable technically but is weak on the regulatory context can create serious problems.

Assess Technical Strengths and Architectural Readiness

In 2026, fintech users in Singapore expect apps to load instantly and work all the time. Even small delays or outages can damage trust.

- Cloud-Native & API-First: Look for a partner who builds systems using modern cloud technologies like microservices and containerization (Kubernetes). This allows the platform to handle sudden growth – from thousands to millions of users – without downtime.

- Integration Resilience: Modern Fintech platforms depend on third-party APIs like KYC checks, payment gateways, and core banking systems. Your partner must know how to handle failures safely. If an external service goes down, the system should recover smoothly without losing or duplicating transactions.

- AI Governance: If you use AI for fraud detection or credit scoring, your partner must document how the models work. They should test for bias and ensure transparency. This helps you meet regulatory expectations and avoid compliance issues.

The bar for quality and security is high for the CTO’s building, lending, or investment platforms. Robust security measures such as end-to-end encryption, tokenization, secure key management, and monitoring systems must be planned from the beginning, not added later.

Moreover, it is essential to assess whether the chosen partner maintains ISO 27001 certification and has undergone third-party penetration testing for prior clients. Before you go ahead, you must inquire about how they have handled vulnerability disclosure in the past. This step makes you aware of a lot about their security culture.

Verify Security Posture

With cybersecurity emerging as fintech’s primary spending focus in 2026, multilayered protection, i.e., “fortress-level” security, is a non-negotiable differentiator. The following are the approaches that can be used to assess security readiness:

- Design-led Security: During the design phase, examine how they integrate threat modeling and deploy Zero-Trust controls.

- 2026 Security Standards: Verify conformity to PCI DSS v4.0.1 standards, ISO/IEC 27001 frameworks, and regional data localization requirements.

- Next-Gen Authentication: Confirm your partner’s proficiency in deploying phishing-resistant passkeys, liveness detection, and behavioral biometrics to prevent account takeovers.

Structure the Selection Process

Rather than following a transactional outsourcing model, you should focus on long-term resilience and ownership.

“Majority of business leaders say sharing customer insights, technology and industry knowledge is critical to competitive agility” — Accenture study on ecosystems

You can do that with these three non-negotiable filters:

- Define the Build-vs-Buy-vs-Partner Strategy: This decision-making framework helps you source each of the components of your product the way you want. It guides you in keeping proprietary risk logic, credit models, and core IP in-house; outsource commodity infrastructure, such as payment processing, KYC orchestration, and cloud provisioning – where the right partner adds value without exposing core strategy.

- Run a Pilot Sprint: Test the partnership before signing the full contract by conducting a 2-4 week pilot sprint. This allows you to evaluate technical standards and collaboration.

- Validate Exit Readiness: Before diving in, make sure the contract explicitly defines data portability, along with knowledge transfer mechanisms to prevent vendor lock-in.

Selecting the appropriate model for each layer of your stack drives growth and reduces future rework costs, as it is fundamental to sound fintech software development.

Strong vs. Weak Fintech App Development Partners

| Evaluation Area | Strong Partner | Weak Partner |

|---|---|---|

| Compliance Approach | Embedded in the foundation right from the start | Considered something to review once the product goes live |

| MAS Familiarity | Brings up PSA, TRM guidelines, and FEAT standards during discussions | Speaks vaguely about “regulatory awareness” but lacks details |

| Security Standards | ISO 27001 certified, PCI DSS v4.0.1 compliant, third-party pen tested | Promotes security knowledge without verifiable certifications |

| API Integration | Manages failures, retries, and transaction integrity as a standard practice | Builds only for ideal scenarios |

| Pilot Willingness | Agrees to a scoped sprint prior to long-term engagement | Pushes straight to full contract |

| Exit Readiness | Proactively defines data portability and handover terms | Avoids clear commitments on ownership and transition |

| Documentation | Maintained and followed as a core practice across every phase | Delivered under last-minute pressure |

Red Flags to Watch For Before You Finalise

Believe it or not, partnership failures are visible in most cases, even before you sign the contract. This can be avoided if you know exactly what to look for. Listed below are several signals that should give any CTO pause:

Their focus begins with a tech stack, not regulations.When the partner begins the talk with their preferred frameworks instead of understanding your compliance obligations, has their priorities backwards. In fintech, architecture comes after regulation, not the other way around.

Compliance responses lack clarity. When the partner is unable to speak and have vague understanding of MAS TRM guidelines and PSA obligations, then it is a clear indication you should stop and reassess. Besides, ask them how they have handled audit trail requirements in prior builds, because chances are, that flaw will appear when the stakes are highest.

They resist a pilot sprint. A confident, capable team welcomes the opportunity to demonstrate quality on a scoped engagement. Resistance to a pilot is rarely about logistics – it’s about confidence.

Exit terms are an afterthought. If data portability, codebase ownership, and knowledge transfer aren’t raised proactively in commercial discussions, you’re likely looking at a partner whose business model depends on lock-in rather than performance.

Why Intelegain Is Built for Fintech

Intelegain brings deep, specialized experience in fintech app development services that addresses precisely the criteria above. With a track record across digital banking, payments, lending platforms, and wealth management applications, Intelegain combines regulatory awareness with genuine full-stack engineering capability – from core banking integrations and KYC/AML orchestration to mobile-first consumer experiences.

Their engineering approach is built around financial-grade security standards, cloud-native architecture, and delivery practices designed for the compliance and auditability requirements the fintech sector demands. For CTOs in Singapore looking for a development partner who speaks both the business language of financial services and the technical language of scalable, secure systems, Intelegain’s fintech app development services offer a compelling combination of domain depth and engineering rigor.

The right partner doesn’t just build what you specify – they help you specify it better. That’s the standard worth holding to. So, do not wait, reach out to us today and build your fintech product on a foundation that’s engineered to last.

Let’s Build Your Next-Gen Fintech Platform